Banker Tips > Research > Quick & Dirty CRE Listing Assessment

Quick & Dirty CRE Listing Assessment

I’ve said it before and I’ll say it again – time is one of our most precious and limited resources. Some of the best lenders I know are the girls and guys who can quickly assess a deal and determine if it supports the debt being requested. This is an easy method to quickly assess a deal. Does this tell you that a property will definitely be approved for a loan? NO….But what it can tell you is if a property will probably not be approved.

Bankers are not gamblers. But we still need to know when to hold ’em and when to fold ’em.

I love working with commercial properties because there is typically enough information included in the listing to give you a good idea of whether an investment is worth pursuing. The great thing about cap rates on commercial listings is that you get enough information to hopefully understand the basic financials of the property.

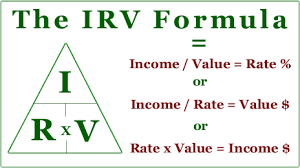

With just a cap rate and a listing price, you can determine the NOI.

As a reminder, the CAP rate or IRV formula:

Cap Rates – You gotta love ’em!

So, as long as you have 2 of the 3 (NOI, Cap Rate, Value) you can determine the 3rd number.

As an example let’s say your borrower has identified a triple-net or NNN single-tenant retail investment property. The lease looks good with 9 years remaining and the tenant is on their second lease renewal so they’ve been there a while – check and check. The property is listed for $2 million and the listing advertises a 7% cap rate.

Using the formula we know that $2,000,000 (Purchase Price) x 7% (Cap Rate) = $140,000 NOI

Let’s say for example that you work at a bank where the minimum DSCR requirement is 1.25x. This means for every dollar of debt, the property is generating $1.25 of income. Simply put, this is a way that lenders can build some “cushion” into the deal so the loan can still be paid in the event that something negatively impacts their income (increased vacancy, decreased rent rate, unforeseen expenses, etc).

Knowing what we do about the property we calculate the following:

$140,000 (NOI)

Divided by 1.25 (minimum DSCR)

= $112,000 (this figure is the maximum allowable annual debt service given the DSCR criteria we have)

So, take that $112,000 and divide it by 12 to get the maximum allowable monthly debt payment of $9,333 or so.

Now, using your financial calculator, plug in your payment along with your typical amortization and interest rates. I assumed a 4.95% rate and a 20 year amortization in my example. This provided me with a maximum loan amount of $1,420,173. If I divide that by 70% (let’s pretend 70% is my bank’s typical max LTV for this type of property), I get $2,028,818. This suggests that a loan at 70% based on the loan criteria I used, would support a maximum property sale price of $2,028,818.

If the max LTV were 75%, then maximum sale price would drop to $1,893,564. This tells you that the borrower would have to put 30% down to make the deal work…25% down will not cut it.

Let’s say they are OK with 30% down…Are you ready to give them an approval?? Not quite yet!

Frankie says RELAX and don’t approve that deal just yet!

Keep in mind that full underwriting could include imputing a vacancy rate as well as reviewing the income statements that were used to determine the cap rate in the listing. Often times, as a lender, you will adjust some of these figures to make the analysis more realistic. As surprised as you may be to hear this, sometimes an agent will make the numbers look really good in an attempt to make the listing look more attractive. I know…it’s shocking…but believe me it can happen.

While you won’t be able to give your client an approval based on this exercise, I can tell you that once you learn this method, it will take about 2 minutes to do on any deal and if you can quickly see whether a deal is worth further analysis.

So there you go…you probably read this article in less than 10 minutes and it should save you a TON of time in assessing CRE deals. Now that you have some extra time you need to get out there, warm your cold calls, preplan for your meetings, avoid these prospecting pitfalls, and close some more deals!